Welcome to the GRBblog! Get to know GRB, Rochester's only locally owned and managed commercial bank. A commercial bank, but also a community bank, with an entrepreneurial spirit about everything we do. We're committed to Growing Rochester Business and making our community a better place to live and work.

The GRBblog is where we post bank news and information, stories about the great organizations we support, and share relevant local and national business news.

GRB is proud to announce that the bank has been recognized by the Independent Community Bankers of America (ICBA) on the 2023 list of “top-performing community banks” in the most recent edition of “Independent Banker” magazine. Ranked at no. 24 in the more than $1 billion asset category, GRB also appeared on the ICBA list in 2021 and is the only New York state bank on the nationwide 2023 list.

ICBA’s calculations aim to recognize community banks that are consistent high performers. Using FDIC data, it looks at pre-tax return-on-assets (ROA) figures from the past three years, with the most recent year weighted at 3x, second most recent year at 2x and third most recent year at 1x. ICBA divides the community banks into three broad segments based on asset size and ranks each segment based on the three-year weighted average ROA. GRB’s three-year average pre-tax ROA of 2.25% puts it among the top 1.88% of community banks in all 50 states. In the northeast, only four community banks were part of this year’s ICBA list of 75.

“Both the uncertainty of the last few years and the recent interest rate increases have taken a toll on the banking industry as a whole. At GRB, we are pleased that the Bank remains strong financially and continues to effectively serve our clients and the local community,” said GRB President and CEO Philip L. Pecora.

Pecora also credits GRB’s continuous technology investments and high-performing workforce with creating a strong culture of service that resonates with local customers.

“Our investment in technology made it possible to react quickly during the pandemic, but it is our people who continue to make sure that our customers receive the superior level of service that sets community banks, like GRB, apart,” said Pecora. “We strive to cultivate a customer-centric, relationship-driven culture at GRB, which is a key factor in the Bank’s ongoing success.”

Over the past three years, GRB was recognized for a number of other accomplishments, including earning Diamond Award status from the U.S. Small Business Administration, being named to the “Greater Rochester Chamber Top 100” list of fastest-growing privately owned companies, and being recognized as one of the “Best Companies to Work for in New York” by the Society for Human Resource Management.

Theft and fraud are problems day to day. But when you travel, the risk can increase. Follow these tips before, during, and after to make sure your money and your identity remain safe and secure while traveling.

Before you leave

Call your bank and credit card companies: Let them know your itinerary to avoid service disruptions. You can also choose to temporarily freeze any financial accounts you won’t need while traveling.

Don’t share your travel plans online: It’s exciting to talk about your upcoming vacation plans on your socials, but you could be giving fraudsters a helpful heads up. Only share your plans with people you trust.

Put your mail on hold: Nothing says, “Nobody’s home” like a stack of mail or newspapers. You can een sign up with the USPS to put your mail on hold using their online portal.

Be prepared

Eliminate unneccessary items from your wallet: Only bring cards and identification that you plan to use. All other identifying information should be removed.

Keep luggage tag info to a minimum: A phone number and last name are adequate to recover lost luggage. Don’t provide thieves with your full address, email address, or other information on your luggage tag.

Copy important documents: Keep copies of important documents in a separate, safe place when you travel. This includes passports, driver’s licenses, credit cards, etc. If anything is misplaced or stolen, these copies will be critical.

Add security options to your devices: Implement multi-factor authentication and set up recovery steps for critical apps. Take advantage of PIN code and biometric scanners on phones, tablets, and laptops. Also, consider installing an app to help locate your devices if they get lost or stolen.

While you are away

Don’t share your itinerary in real time: Again, social media accounts contain a treasure trove of information that can be used to steal your identity or even plan a theft of your home or hotel. Continue to be cautious about what you post on your socials.

Think safety first when accessing cash: When using ATMs, try to find ones that are monitored by security cameras or secured in a bank lobby. This will reduce the risk that a skimmer has been installed in the ATM or that thieves can watch your transaction.

Avoid using public WiFi for financial transactions: Be careful when using public WiFi. Identity thieves may try to hack these connections and steal your personal information.

Lock up important documents and valuables: If your vacation stay has a safe, use it. Lock up important documents, jewelry, devices, identifiable information, and extra cash and credit cards.

When you return

Review your bank and credit card account statements: Make sure you can identify all the charges and that the dates and locations match up with your itinerary. If they don’t, contact your bank or credit card company immediately. Don’t forget to let your bank and credit card companies know you’ve returned from your vacation.

Update account passwords: If you were forced to access any of your accounts from a public computer or public WiFi, change the passwords on those accounts for added security.

Shred sensitive documents: While some of your recipts may recall fond memories of your travels, they also contain important private information. Consider shredding items such as boarding passes, flight itineraries, and rental receipts.

Vacation should be a relaxing and wonderful experience, but to stay safe and secure while traveling requires special attention. For additional information on fraud and security, check our website. If you have any concern about fraud on your GRB accounts, please call us or contact us online.

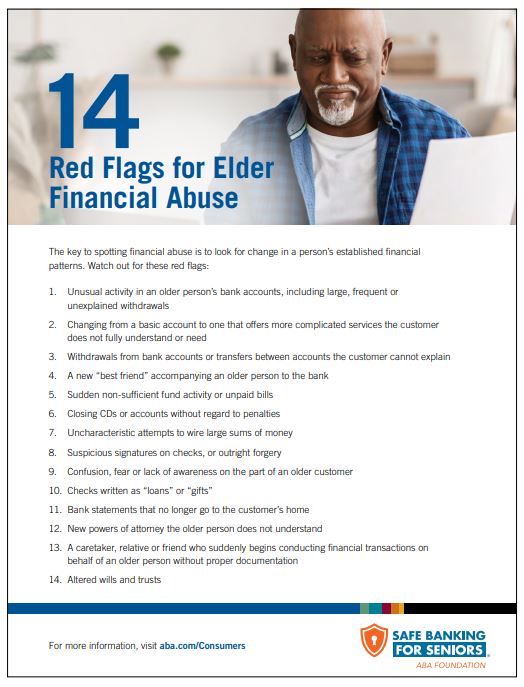

Today is Senior Fraud Awareness Day. GRB has teamed up with the American Bankers Association Foundation to help older adults, families, and caregivers prevent elder financial abuse and exploitation with the Safe Banking for Seniors program. #SafeBankingForSeniors

According to the Alzheimer’s Association, 10-20% of elders 65 and older have some type of mild cognitive impairment. Mild cognitive impairment causes a slight deterioration of cognitive abilities, which may affect memory, thinking, and reasoning skills. This can make it easier for them to become victims of fraud.

Types of Fraud

Scams impacting older adults can involve lotteries, sweepstakes, identity theft, home improvement and repair, telephone donation calls, healthcare and prescription drugs, dating, and more.

Financial institutions have protections in place designed to miminize elder financial abuse. In New York state, the Office of Children and Family Services has oversight on elder abuse and provides the following resources for prevention and reporting:

If you suspect someone may be a victim of elder abuse, contact your local Department of Social Services Adult Protective Services office by searching online or calling 1.800.342.3009, press 6.

We are pleased to announce GRB has ranked no. 4 in the the medium employer (100-249 employees) category for “Best Companies to Work For New York.” We moved up a spot from 2022 and we are so proud of our employees for making GRB a great place to work for the ninth consecutive year.

“The 2023 Best Companies to Work for in New York are champions of business who know the importance of a positive, productive work environment. They support their staff members which results in success throughout the entire company,” said Suzanne Fischer-Huettner, managing director of BridgeTower Media. “The Rochester Business Journal is pleased to join the New York State Council of the Society for Human Resource Management and the Best Companies Group in recognizing the achievements of these deserving companies.”

Awards for the “Best Companies” are based on feedback provided through employee surveys, which focus on:

Leadership & Planning

Corporate Culture & Communications

Role Satisfaction

Work Environment

Relationship with Supervisor

Training, Development & Resources

Pay & Benefits

The survey process is managed by Best Companies Group (BCG) and winners are published by New York State SHRM (NYS-SHRM).

“This year’s Best Companies to Work for in New York know the importance of communication, onboarding, feedback loops, flexibility, and diversity and inclusion in a successful work environment. They make sure their staffers feel appreciated, engaged and successful,” said Suzanne Fischer-Huettner, managing director of BridgeTower Media. “Along with our partners, the New York State Council of the Society for Human Resource Management and the Best Companies Group, we are honored to recognize the accomplishments of these outstanding businesses.”

On behalf of the whole team at GRB, we want to thank our customers and partners for being part of our ongoing growth as we support individuals, families and small businesses in Western and Central New York.

Small businesses are a vital part of the American economy, and community banks play a crucial role in supporting these businesses. Genesee Regional Bank provides personalized service and a demonstrated commitment to our region. We understand the unique qualities of our community and work hard to provide products and services that support its growth and development.

This year, we celebrate Community Banking Month with a particular focus on what sets us apart and makes us a vital part of the community’s financial infrastructure.

The Impact of Community Banks

According to recent data, community banks account for a significant portion of small business lending. In fact, community banks provide over half of all small business loans, despite holding only 16% of total banking assets.

GRB provides small business lending through U.S. Small Business Administration loans and our own portfolio. Unlike larger banks, we often have more flexibility when it comes to the loans we make. We consider critical factors such as local market conditions, past experience, and the potential for growth when making our lending decisions.

In addition to providing financing, community banks also offer valuable resources and support to small businesses. Our local business networks connect small business owners with other businesses in the area. Our goal is to help each and every business succeed.

Neighbors, Businesses, Communities

Small businesses remain the backbone of our economy, and community banks support them. By providing personalized service, flexible lending options, and valuable resources, community banks play a critical role in helping small businesses grow and thrive.

If you are a small business owner in need of financing or other resources, try a community bank, like GRB. You might find that our individualized approach and local knowledge can be a valuable asset in securing the right lending and deposit options. At GRB, we are Here. For You.

Find out more about Community Banking Month by following GRB’s unique customer visits featured on our website and social channels throughout the month of April.

Stacey MichaelsMonday, February 27, 2023Uncategorized

February 27th – March 3rd marks this year’s America Saves Week, a campaign to bring awareness and education to everyday Americans about saving successfully. Each year, thousands of organizations participate, representing a diverse and impressive coalition of companies, nonprofits, educational institutions, military services, influencers, government agencies, and financial institutions. The week encourages individuals and families to assess their financial well-being, which helps them build a clear picture of how they can stay prepared for the unexpected and make progress toward their goals.

The theme for America Saves Week 2023 is, “A Financially Confident You.” But financial confidence is much more than just how much is in your bank account. Financial confidence is a combination of financial literacy, education, resources, and more. They all play a part in securing your financial future, no matter what your unique circumstances might look like.

Each day during the week has it’s own topic and with it different things to think about. How can I incorporate automatic savings into my regular habits? What major milestones am I saving for? Or how can I jumpstart a new savings journey when I’m ready to take control of my finances?

Below you’ll find the list of each day’s topic, as well as links to resources to help you learn more about how you can improve your financial well-being through saving.

America Saves Week Daily Themes:

Monday, February 27 – Saving Automatically – check out the America Saves blog post on the simplest way to save!

Tuesday, February 28 – Saving for the Unexpected – learn more about staying prepared on today’s blog post!

Wednesday, March 1 – Saving for Major Milestones – this blog post has all the tips you need on saving for the big moments!

Thursday, March 2 – Paying Down Debt is Saving – today’s America Saves blog talks how to approach dealing with debt.

Friday, March 3 – Saving at Any Age – read up on the ongoing journey of saving here!

Stacey MichaelsWednesday, February 22, 2023GRB Mortgage

Today, the Department of Housing and Urban Development’s (HUD) announced a 30 basis point reduction to the Annual Mortgage Insurance Premiums (annual MIP) it charges borrowers for Federal Housing Administration (FHA)-insured single family mortgages. Aimed at helping make homeownership more accessible and affordable for the nation’s homebuyers, the reduction in mortgage insurance will be effective for mortgages endorsed for FHA insurance on or after March 20, 2023.

According to the FHA, this reduction will benefit approximately 850,000 borrowers over the coming year, saving them $678 million in aggregate in the first year of their FHA-insured mortgage. For the average borrower purchasing a one-unit single family home with a down payment of 3.5 percent and a mortgage amount of $467,700 – the national median home price as of December 2022 – FHA’s annual MIP reduction will save them more than $1,400 in the first year of their mortgage.

Given the nationwide housing shortage, the move is seen as an encouraging one by those in the industry.

“The lower premiums will expand homeownership opportunities by lowering mortgage payments for qualified FHA borrowers, providing critical relief from the steep rise in mortgage rates and home prices just in time for the spring buying season,” said Mortgage Bankers Association President and CEO Bob Broeksmit, CMB, in a statement. “This will especially help minority homebuyers and low-and moderate-income households who are predominantly served by FHA loans.”

FHA mortgage insurance facilitates broader availability of mortgage financing to those not adequately served by the conventional mortgage market. More than 80% of FHA borrowers are first-time homebuyers.

We are proud to announce that GRB President and CEO Philip L. Pecora was named to the Rochester Business Journal’s Power 100 List for 2023. The Power 100 recognizes community leaders making a positive impact on the Greater Rochester region.

Leadership in the Region

President and CEO Philip L. Pecora

According to RBJ Associate Editor and Publisher Ben Jacobs, “As with last year, the mix of industries represented is no surprise.

“The health care industry and the nonprofit sector, which are heavily intertwined in Rochester, have faced significant challenges over the past three years and many leaders from these areas appear on this list.

“Banking and finance, education, law, manufacturing, technology, and real estate and construction also have a significant presence here and in our local economy.

“Over the rest of the year, as we did last year, we will delve deeper into several of these industries — banking and finance, accounting and insurance, health care, law, real estate and construction — with Power 30 lists that will allow us to highlight more people who are working to make an impact in Rochester.”

GRB’s Growth

GRB was established by Founders E. Philip Saunders and partner Dan Gullace in 1996. Their goal was to re-establish a community bank presence and grow small business in the Rochester area. Since that time the bank has continued on a consistent growth path with more than a billion dollars in assets.

Under Pecora’s leadership, GRB spent the last three years focusing on bringing financial stability to small businesses and consumers. The bank supported the small business community during the Paycheck Protection Program and earned a Gold Award from the U.S. Small Business Administration for its small business lending activities last year.

We are proud of GRB’s community commitment and proud to have Pecora’s efforts recognized as part of the Power 100.

Read more on Phil’s Power 100 profile on the RBJ website.

Stacey MichaelsWednesday, February 1, 2023Community

This month GRB is celebrating the contributions that Central and Western New York’s Black leaders have made in creating a diverse and inclusive culture. While we acknowledge that the journey for equality is ongoing, we are proud to be part of communities with vibrant and longstanding histories of Black leadership.

In Rochester, we are fortunate to be able to draw inspiration from the generational progress that began with Frederick Douglass. Rochester’s Frank Stewart started the first Black baseball team in 1866 and Hester C. Jeffery founded the Susan B. Anthony Club for Colored Women in 1891. We are also proud to celebrate Beatrice Amaza Howard, the first Black woman to graduate from the University of Rochester in 1931 and Rochester’s own Cab Calloway, a Grammy award-winner and gifted entertainer. We acknowledge the accomplishments of Kathryn Green Hawkins, the first Black woman to join the Rochester Police department. Hawkins served first as an officer in 1956 and was subsequently promoted to lieutenant in 1964.

In Syracuse, the Harriet Tubman National Historical Park recognizes one of the Underground Railroad’s most iconic figures. Syracuse also celebrates Sarah Loguen Fraser, the daughter of Underground Railroad conductors and the first Black woman to graduate from the Syracuse University College of Medicine. Syracuse Stars baseball player Moses Fleetwood Walker was actually the first Black man to play professional baseball. In 1884 he played for the Toledo Mud Hens and later the Syracuse Stars. After Moses, professional baseball remained segregated until Jackie Robinson broke the color barrier in 1947. Syracuse University also boasts the accomplishments of Ernie Davis, the first Black player to win the Heisman Trophy in 1961.

Activities to Celebrate Black History Month

We know that our Western and Central New York cities would not be the diverse ecosystems they are today without the perseverance of Black leaders who chose to contribute their considerable talents in the communities we call home. In celebrating the past, we hope to find the inspiration to continue moving forward.

Stacey MichaelsMonday, January 30, 2023GRB Mortgage

As a bank, GRB is able to work with the Federal Home Loan Bank of New York (FHLBNY) to provide grant assistance to qualified first-time homebuyers. The Homebuyer Dream ProgramTM provides grants of up to $10,000 towards the purchase of a home in New York. This is a program that is only available to banks, mortgage brokers are not able to access grant funds for this program.

The FHLBNY uses an allotment program, providing lenders with a set amount of funding.

The program begins accepting applications for funds on March 27, 2023.

Have a household income at or below 80% of area median income (i.e., in Monroe and Onondaga county, 1 or 2 person households, up to $79,600. In households of more than 3 people, the maximum income level is now $91,540)

Complete an accredited homeownership course

Meet the income and credit requirements for the program

Have the minimum equity contribution of $1,000 toward purchase of the home

Remain in the home for five years or repay a portion of the grant funds back to FHLBNY

Important information

Up to $9,500 in grant funding is available to be applied to down payment and closing costs

Up to $500 in grant funding is available to offset the cost of the homeownership course

Please note, the information in this post refers to the 2023 HDP. The Federal Home Loan Bank of New York assesses the HDP on an annual basis and the program is subject to change. Please go to our Mortgage Loans page for more information on the HDP and other grant and lending options.

*Homebuyer Dream Program is a trademark of the Federal Home Loan Bank of New York.

**First-time homebuyer as defined by the U.S. Department of Housing and Urban Development (“HUD”), is an individual who meets any of the following criteria:

An individual who has had no ownership in a principal residence during the 3-year period ending on the date of the purchase of the property. This includes a spouse (if meets the above test, they are considered first-time homebuyers).

A single parent who has only owned a principal residence with a former spouse while married.

Individual who is a displaced homemaker and has only owned a principal residence with a spouse.

An individual who has only owned a principal residence not permanently affixed to a permanent foundation in accordance with applicable regulations.

An individual who has only owned a property that was not in compliance with state, local or modelbuilding codes and could not be brought into compliance for less than the cost of constructing a permanent structure.