Welcome to the GRBblog! Get to know GRB, Rochester's only locally owned and managed commercial bank. A commercial bank, but also a community bank, with an entrepreneurial spirit about everything we do. We're committed to Growing Rochester Business and making our community a better place to live and work.

The GRBblog is where we post bank news and information, stories about the great organizations we support, and share relevant local and national business news.

The Federal Housing Finance Agency (FHFA) has announced new maximum conforming loan limits for 2024.

In Central and Western New York:

The maximum conforming FHFA loan limit for one-unit properties will be $766,550. This is an increase of $40,350 over the 2023 limits.

Multi-family property conforming limits also increased. Two-family properties are up to $981,500 and three-unit homes are up to $1,186,350. The new limit for four-unit properties is $1,474,400.

The Housing and Economic Recovery Act (HERA) requires that the baseline conforming loan limit be adjusted each year for Fannie Mae and Freddie Mac. The adjustment reflects changes in the average U.S. home price. The percentage increase in the maximum conforming loan limit follows the Housing Price Index for the prior four quarters.

“The annual FHFA adjustment is an important tool for homebuyers,” said GRB’s SVP, Residential Mortgage Manager Mike Pulver. “The additional boost in limits provides better financing options for loans that would traditionally have fallen into the ‘jumbo’ category.”

For new loan applications or applications already in process, the loan amounts will be subject to 2023 limits as long as the loan closes by Dec. 31. Loans closing on Jan. 1 or after will fall under the 2024 limits.

FHA loan limits are expected to increase as well. We will post updates as they become available.

We’re proud to have GRB President and CEO Philip L. Pecora interviewed in the Rochester Business Journal about the use of technology and how the bank provides a personalized customer experience.

President and CEO Philip L. Pecora

Of particular note, the article points out that in Leadsquared’s Top 10 Digital Banking Trends for 2024, customer experience that is hallmarked by personalization and simple, consistent interaction “is everything.” And a 2023 survey by Statista of more than 75 thousand banking consumers found that good old-fashioned trust was the most valued aspect of banking.

“We truly keep banking simple,” said Pecora. “We are very focused on delivering core banking products that we are very good at delivering – first and foremost personally, but also supported digitally. Our banking service centers on a personal relationship between our bankers and our valued clients, while the transactional aspect of a product or service is often efficiently facilitated through technology.”

“We use technology to leverage our personal interactions, not replace it,” he added.

“Technology is a must-have in the banking business; however, it is the personal relationships driven through local and autonomous decision-making that differentiates GRB from the larger, less personal financial institutions,” said Pecora.

Stacey MichaelsThursday, November 9, 2023GRB Mortgage

As a bank, GRB is able to work with the Federal Home Loan Bank of New York (FHLBNY) to provide grant assistance to qualified first-time homebuyers. The Homebuyer Dream ProgramTM provides grants of up to $20,000 towards the purchase of a home in New York. This is a program that is only available to members of the FHLBNY, mortgage brokers are not able to access grant funds for this program.

The FHLBNY uses an allotment program, providing lenders with a set amount of funding for the year. Funds are distributed to homebuyers on a first come, first serve basis.

The program begins accepting applications for funds on January 8, 2024, several months earlier than in past years.

This means it is critical that prospective Homebuyer Dream applicants begin working with their GRB mortgage originator now in order to be ready to apply when the program opens. GRB has team members able to serve residents throughout Western and Central New York.

Reside in and be purchasing a home in New York state

Have a household income at or below 80% of area median income

Complete an accredited homeownership course

Meet the income and credit requirements for the program

Have the minimum equity contribution of $1,000 toward purchase of the home

Remain in the home for five years or repay a portion of the grant funds back to FHLBNY

Important information

Up to $19,500 in grant funding is available to be applied to down payment and closing costs

Up to $500 in grant funding is available to offset the cost of the homeownership course

Please note, the information in this post refers to the 2024 HDP. The Federal Home Loan Bank of New York assesses the HDP on an annual basis and the program is subject to change. Please go to our Mortgage Loans page for more information on the HDP and other grant and lending options.

*Homebuyer Dream Program is a trademark of the Federal Home Loan Bank of New York.

**First-time homebuyer as defined by the U.S. Department of Housing and Urban Development (“HUD”), is an individual who meets any of the following criteria:

An individual who has had no ownership in a principal residence during the 3-year period ending on the date of the purchase of the property. This includes a spouse (if meets the above test, they are considered first-time homebuyers).

A single parent who has only owned a principal residence with a former spouse while married.

Individual who is a displaced homemaker and has only owned a principal residence with a spouse.

An individual who has only owned a principal residence not permanently affixed to a permanent foundation in accordance with applicable regulations.

An individual who has only owned a property that was not in compliance with state, local or modelbuilding codes and could not be brought into compliance for less than the cost of constructing a permanent structure.

Stacey MichaelsFriday, October 20, 2023GRB Employees

Congratulations to Genesee Regional Bank’s (GRB) President and CEO Philip Pecora on being named to the Rochester Business Journal’s (RBJ) Power 30 Banking & Finance 2023 list.

From the RBJ’s Associate Publisher and Editor Ben Jacobs, “The people on this list have helped Rochester’s banking and finance industry navigate COVID-related uncertainty, significant supply chain and labor disruptions, increases in interest and inflation rates, and unpredictable economic conditions. They have kept their clients apprised of new rules and regulations, financing options, investment opportunities and more. They have pushed innovation forward to deal with myriad challenges and have led the way through a period of tremendous uncertainty.”

GRB President and CEO Philip Pecora

Leadership through change

Under Pecora’s leadership, GRB has shown steady growth. While Fed rate hikes over the last 18 months have been a significant challenge for the banking industry as a whole, Pecora remains optimistic.

“The Greater Rochester economy was resilient through the pandemic and has shown continued strength through this rising interest rate environment. Our local businesses’ balance sheets are strong, unemployment is low and housing values have stabilized. As a result, there has been a resurgence of community banks in our area who are interested in serving our local businesses and residents. Our recent history of stability as a reinvented, diverse small business town makes our community an attractive place to bank,” said Pecora.

Building on our strengths

According to Pecora, one of the key’s to GRB’s continued growth is the bank’s unique focus on providing products and services for Upstate New York businesses, residents, and homebuyers.

“I’m a Rochester native and I’m proud of how this community continues to evolve. At GRB, we do the same,” said Pecora. “Being privately owned by local entrepreneurs, we at GRB certainly are excited to call Rochester our home and look forward to continuing to grow with our valued clients and greater community.”

This strategy has led GRB through both opportunities and challenges, with the bank appearing on both the Greater Rochester Chamber of Commerce Top 100 list and the Best Companies to Work for in New York list. In 2020, Standard & Poor Global Market Intelligence named GRB one of the “Best-Performing Community Banks for 2020.” Ranking at no. 23, GRB was the only bank in New York state on the national list. GRB was also recognized by the Independent Community Bankers of America (ICBA) as one of the “top-performing community banks of 2023.” Again, GRB was the only New York state bank on the nationwide list.

Read the full article the Power 30 on the RBJ website.

Stacey MichaelsWednesday, October 11, 2023Uncategorized

October is Fire Prevention Month and this week, October 8-14, is Fire Prevention Week. Since 1922, the National Fire Protection Association (https://www.nfpa.org/) has sponsored the public observance of Fire Prevention Week. In 1925, President Calvin Coolidge proclaimed Fire Prevention Week a national observance, making it the longest-running public health observance in our country. During Fire Prevention Week, children, adults, and teachers learn how to stay safe in case of a fire.

Genesee Regional Bank is not only committed to helping people in our community find the home of their dreams, but also to keep those homes safe so they can continue making memories in them for years to come. We’re fortunate to have some of our own employees serve in the community as volunteer firefighters. Information Security Analyst Joel Kaigler and Vice President, Sr. Commercial Relationship Manager Denis Jefferies provided us with a few tips on keeping your home and family safe from fires and carbon monoxide:

Check Your Smoke & Carbon Monoxide Detectors

First and foremost, check smoke detector batteries and put detectors in every room and sleeping area. It’s important to have them on every level of your home and perform regular testing once a month to ensure the detectors are functioning properly. You should replace your smoke detectors around every 10 years from the manufacture date. Depending on your municipality, the local fire department may have a program to install these and/or provide them for you free of cost, so check to see if a program is offered in your area.

Second, install carbon monoxide (CO) detectors in your home. Carbon monoxide is produced by various fuel burning appliances (gas stoves, gas furnaces, fireplaces, etc.). If those appliances aren’t venting properly, it can create a dangerous buildup of the gas inside your home. Carbon monoxide is lighter than air, so you want to put your detectors around 3-5 feet off the ground. Install these detectors in a garage, outside sleeping areas, and in the basement (but be careful not to place them near any gas burning appliances which can produce false positives). If your carbon monoxide detectors go off, call 911 and evacuate with your family and pets until the fire department arrives.

Have an Exit Plan

In the event of an actual fire or gas leak, it’s crucial to develop an exit plan and review the plan with all the members of your family. You’ll want to review with all family members how to exit the home and get to a meeting spot somewhere out of danger and away from the structure. With younger children, it’s important to take them to a fire department open house and let them see firefighters in full gear, if possible. Once fully masked and suited up, firefighters can look frightening to younger kids, so having a chance to be exposed to them in a friendly setting can prepare children in case of an emergency.

Make Your House Number Visible

Finally, another item that can save valuable time when emergency help is called to your home is making your house number as obvious to see as possible. Replace house numbers that are too small or are falling off or in bad condition. It may not be top of mind, but you want emergency responders to be able to identify the house, park, and go inside to help – because seconds really do count.

At GRB, we are proud to provide this important information and recognize the extraordinary work of Denis, Joel, and the rest of our community’s emergency responders during Fire Prevention Month – and always.

In 2021, Congress enacted the Corporate Transparency Act. This law creates a Beneficial Ownership Information (BOI) reporting requirement as part of the U.S. government’s efforts to make it harder for bad actors to hide or benefit from their ill-gotten gains through shell companies or other opaque ownership structures.

New requirements start Jan. 1, 2024

Beginning on January 1, 2024, many companies in the U.S. will have to report information about their beneficial owners. Beneficial owners are the individuals who ultimately own or control the company. Companies must report will report the information to the Financial Crimes Enforcement Network (FinCEN). FinCEN is a bureau of the U.S. Department of the Treasury.

Generally speaking, companies structured as corporations, LLCs, and those created by filing a document with the secretary of state or similar office under the law of a State or Indian tribe are likely required to report BOI. For the organization, BOI information includes legal names, DBAs, addresses, TIN, and other basic information.

The information being collected for individual beneficial owners helps establish the identity of the individual. It includes birth date, residential address, and identifying number and image of government-issued documentation (driver’s license, passport, etc.). For reporting entities, a beneficial owner is defined as an individual who either directly or indirectly:

Exercises substantial control over the reporting company (i.e. senior officer, important decision makers, individuals with appointment or removal authority), or

Owns or controls at least 25% of the reporting company’s ownership interests (i.e. equity, stock, voting rights, convertible instruments, capital or profit interest, options, and the like)

Additional resources

The reporting requirements for BOI are not difficult to understand. But there are some fine points that businesses should be aware of as they begin the process. It could also take some time to assemble the documentation required. So it is advisable that businesses develop a reasonable plan for completing their submission.

FinCEN has created a number of materials to assist in the transition, including guides and videos. Although the system being developed by FinCEN to collect the information is not available yet, their guides should be helpful in assisting business owners as they determine their status for beneficial owner reporting. We’ve included the links below to help you get started:

Consumer protection, business, risk management, and insurance professionals all point to the same conclusion when it comes to check fraud:

Check fraud is not something that can be avoided. It is something you and your business will need to address.

Rising numbers

According to the 2023 AFP Payments Fraud and Control Survey, 65% of organizations were victims of payment fraud attacks. Of those, 63% of cases involved fraud activity via checks.

Check fraud does not discriminate by type of business or geography. Last year, criminals targeted more than 25 GRB customers for over half a million dollars in attempted check fraud. Positive Pay caught and deescalated all of these attacks.

Check washing is one of the oldest tricks in the book, but with the rise of new video-sharing apps, such as TikTok, a would-be scammer can learn a variety of methods to wash a check in the time it takes to read this article.

In 2022, businesses lost more than $8.8 billion dollars to check fraud, according to the Federal Trade Commission. That represented an increase of 30% from 2021.

Check fraud does not discriminate by type of business, size of business, or geography.

Preventing Check Fraud with Positive Pay

The best thing you can do to prevent check fraud is to stop writing checks. Of course, this is not always possible when running a business. The second-best thing you can do is enroll in Positive Pay.

GRB offers Positive Pay, free of charge, to all commercial banking customers. It safeguards against check fraud by implementing a system of validation by cross-referencing them against a pre-approved list of issued checks. Any discrepancies in the checks being cashed are flagged for review by Positive Pay. A business can review Positive Pay items can happen from anywhere in the world, via your mobile device or computer, in a matter of seconds.

Positive Pay is simply the best defense against check fraud, and it costs nothing to enroll. Contact your GRB Relationship Manager or our Commercial Relationship Associate Team for more information about Positive Pay.

Criminals continue to find creative ways to attack businesses. Positive Pay makes sure that every check cashed is one actually written by your business.

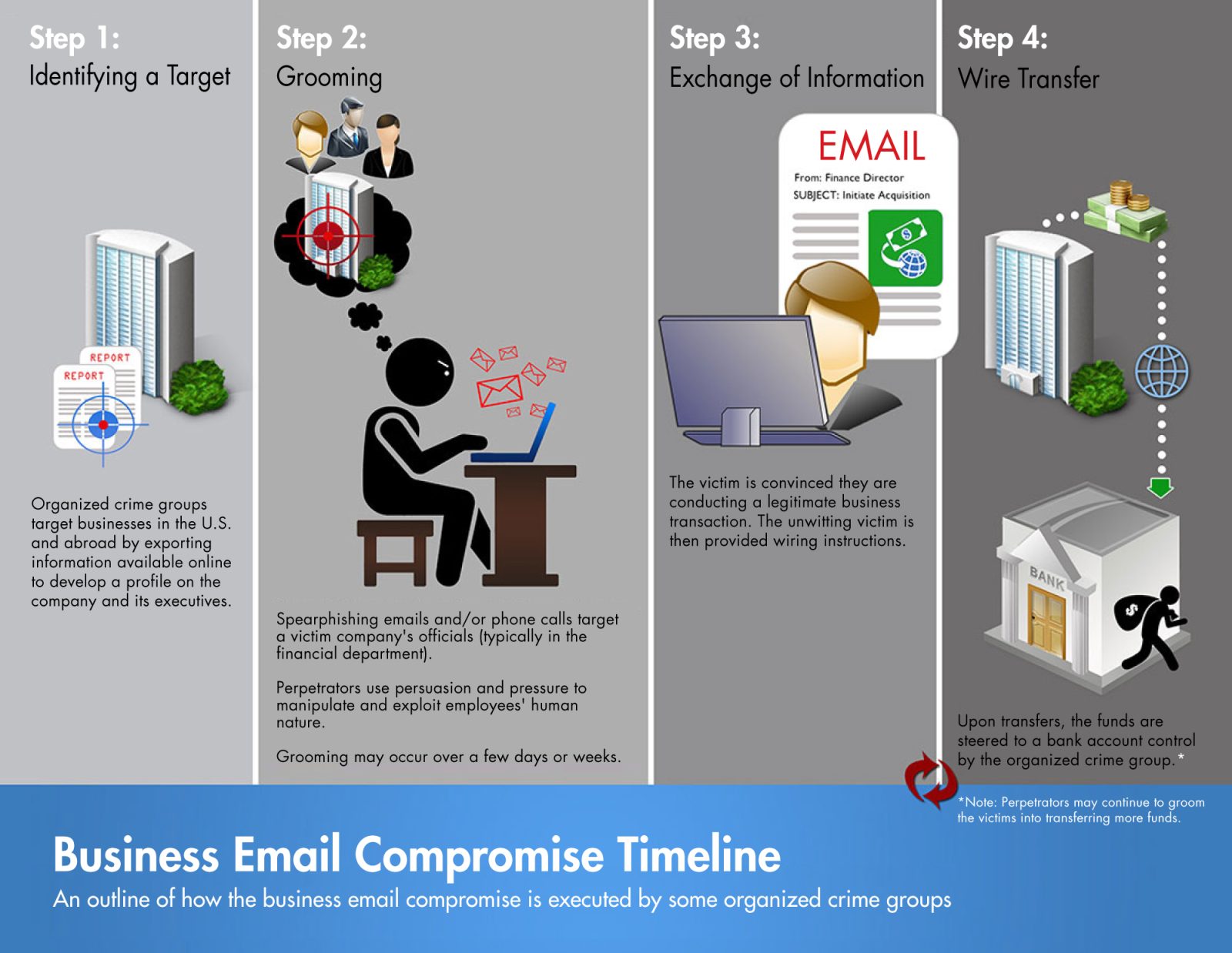

The average amount a company loses to a Business Email Compromise (BEC) attack

Business Email Compromise (BEC) is one of the most financially damaging online crimes. With losses topping more than $2.7 billion last year and a year-over-year increase in attacks of 14.5%, BEC is a significant threat.

What is BEC?

In a BEC scam, criminals send an email message that appears to come from a known source making a legitimate request, like these examples:

A vendor your company regularly deals with sends an invoice with an updated mailing address or account information.

A company CEO asks her assistant to purchase dozens of gift cards to send out as employee rewards. She asks for the serial numbers so she can email them out right away.

A homebuyer receives a message from his title company with instructions on how to wire his down payment.

Versions of these scenarios happened to real victims. All the messages were fake. And in each case, thousands—or even hundreds of thousands—of dollars were sent to criminals instead.

How BEC Works

In this graphic provided by the Federal Bureau of Investigation (FBI) a BEC attack is conducted through careful research to identify targets, groom company representatives, make the request, and finally, secure a fraudulent payment.

Scammers do their homework to make their communications sound believeable. They may research company executives’ social media accounts and reference company posts to make their demands sound more realistic.

But in most cases, breaking up a BEC attack is as simple as picking up the phone to verify instructions or reading between the lines to see if an email really “sounds like” the person you know. BEC attacks are preventable. The ABCs below provide a good start for minimizing your company’s risk.

A

Avoid

Do not use free web-based email accounts or personal email accounts for business – Don’t use free web-based email accounts for business or get in the habit of using personal email accounts to send business emails. Stick to your corporate email account, which should have more stringent security protocols.

Avoid replying to emails – Don’t REPLY, use FORWARD instead. Forwarding an email requires you to manually type the address or select a known, trusted email address from a list. This eliminates a habit BEC attackers depend on to pull off their scams.

B

Be proactive

Implement multi-factor authentication for your business email – MFA makes it much more difficult for cybercriminals to even gain access to an email account that could be used to commit fraud.

Secure your company domain – BEC attacks often use spoofed domains. Registering domain names similar to your company’s will help prevent the email spoofing at the heart of many successful BEC attacks.

C

Check and double-check

Know your customers, fellow employees, and vendors – If something seems off, it probably is. Did a trusted vendor you talked to just last week suddenly email you to say they’ve moved and to send checks to a new location? Is your normally friendly CEO suddenly sending demanding, high-pressure emails requiring money be wired within the hour? Always double-check requests that seem unusual.

Make the call – Don’t email, pick up the phone and call your customer, co-worker, or vendor to verify any unusual requests. Use a known phone number (not one from an email) to verify that a request is legit.

As is the case with most cybercrimes, it’s much easier to prevent a BEC attack than to recover from one. In addition to the financial loss, victims of a BEC attack can end up tied up in lawsuits with customers, vendors, and insurers for years. The cost in time, resources, and reputation warrants taking a few extra seconds to follow the ABCs and keep your business safe.

The Linked Deposit Program (LDP) helps existing New York State firms obtain reduced-rate financing so they can undertake additional investments in their business. GRB has completed a number of these loans successfully and it can be an option for qualifying organizations lower their interest costs and move forward on business objectives.

Businesses commonly use LDP to:

Improve their competitiveness

Expand their markets

Develop new products

Introduce new technologies

Facilitate ownership transition

Modernize their equipment, increase their capacity or capabilities

Expand their facilities, purchase real estate or make building renovations

How it works

Eligible businesses obtain loans from their bank and the New York Business Development Corporation.

New York State places a deposit for the same amount as the loan at the bank and earns less interest on the deposit, allowing the lender to transfer the interest rate savings on to the borrower. At the end of the four year term of Linked Deposit assistance, the bank returns the deposit to New York State.

For lenders, LDP provides a number of advantages that makes lending to eligible businesses more favorable.

Program limits

An eligible business can have an unlimited number of LDP loans outstanding, totaling $6 million.

The single deposit limit has been increased to $4 million; there is no minimum deposit.

Total lifetime assistance (including renewals and prior deposits) cannot exceed the legislated lifetime maximum of $6 million.

Who qualifies?

An eligible business can have an unlimited number of LDP loans outstanding, totaling $6 million.

The single deposit limit has been increased to $4 million; there is no minimum deposit.

Total lifetime assistance (including renewals and prior deposits) cannot exceed the legislated lifetime maximum of $6 million.

If interest rates have been pushing off plans for expanding your business or adding a new product or service and you qualify, LDP can be a great way to secure the funding needed to meet your goals. Contact GRB’s Commercial Banking Team for more information.

At Genesee Regional Bank, we want to recognize E. Philip Saunders for all that he does for not only for the bank, but for the community. As a founder and chairman for numerous influential organizations, including GRB, Saunders has played a pivotal role in contributing to the Finger Lakes Region as a businessman and philanthropist.

Saunders was recently acknowledged for advancing a transformative project for the Finger Lakes Region. Featured in Life in the Finger Lakes magazine, the Saunders Foundation made a generous contribution to an up-and-coming museum that will exhibit the culture and natural history of all the Finger Lakes. The museum’s exhibition hall will be expanded and officially named the Saunders Finger Lakes Museum.

The museum stands dedicated to celebrating the cultural and natural history of the area, situated on a breathtaking 30-acre campus along Keuka Lake in Branchport. The Saunders Finger Lakes Museum offers visitors an array of experiences, including wetlands, walking trails, lake views, paddling programs, a children’s natural playscape, and an outdoor exhibit showcasing the region’s 11 lakes. Construction of the new main exhibition building is set to commence after planned demolition and site preparation in the upcoming fall.