Welcome to the GRBblog! Get to know GRB, Rochester's only locally owned and managed commercial bank. A commercial bank, but also a community bank, with an entrepreneurial spirit about everything we do. We're committed to Growing Rochester Business and making our community a better place to live and work.

The GRBblog is where we post bank news and information, stories about the great organizations we support, and share relevant local and national business news.

The last 30 days have represented a time of change in the Rochester housing market. Coming off two prior years characterized by low inventory, multiple bids, and way-over-asking-price offers, many potential buyers became frustrated and simply put their home ownership dreams on hold. But change – and opportunity – may be on the horizon.

Mike Pulver SVP, Residential Mortgage Manager

Although anecdotal at the moment, GRB’s mortgage team is seeing a small, but important shift in the market. This could be good news for buyers, especially those counting on grant and discount programs or government-backed loans – like Federal Housing Authority (FHA) and Veterans Administration (VA) – to secure financing and get an offer accepted.

“It has been a very difficult market for many buyers over the last two years. Rochester has been an exceptionally hot real estate market and buyers with 20% down or the ability to make a cash offer certainly had an advantage,” said GRB’s SVP, Residential Mortgage Manager Mike Pulver. “Many buyers were priced out of the market by overbidding or lost out to conventional or cash financing offers. So, many well-qualified potential buyers just put their purchase plans on hold.”

Getting Back on the Horse

In fact, buyer pessimism grew more prevalent for homebuyers in July, with the Fannie Mae Home Purchase Sentiment Index (HPSI) falling to its lowest level in 11 years. But that broad feeling of pessimism may be a key reason for smart buyers to begin actively searching again and “get back on the horse.”

“If people have backed away from looking for a home, there may be less competition for the available inventory. We’re seeing a couple of favorable conditions start to emerge for buyers across the board,” said Pulver. “It’s too early to call it a trend, but it may be an opportunity.”

So, what has changed?

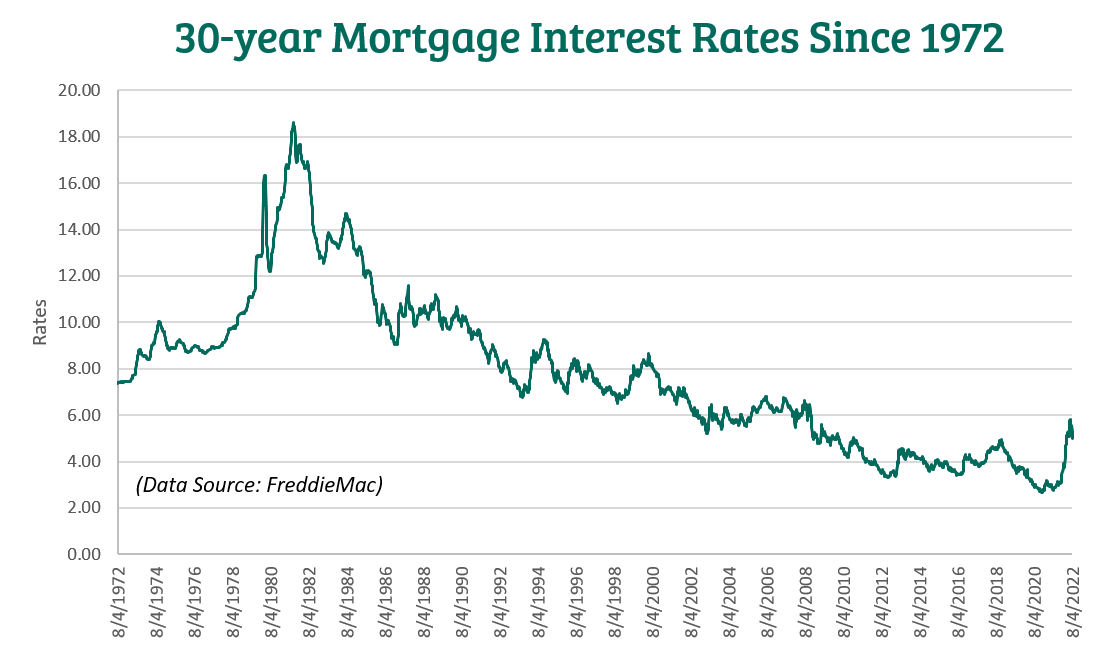

Even with the recent uptick, rates for 30-year mortgages remain among the lowest in the last 50 years.

Fed Rate Hikes – While these increases traditionally have more of an impact on short-term lending rates, the boost has helped cool the mortgage market, too. While this did lead to an increase in mortgage rates, recent activity has seen rates pull back a bit. Historically today’s rates, hovering between 5.50% and 6.00% (as of 8/10/22) for a 30-year mortgage, are still very favorable.

Housing Inventory Increases – Inventory levels may have hit their lowest point and could be inching upward. More homes to purchase means less demand for each home. For potential buyers, this means fewer bidding wars and a better possibility of getting an offer accepted using a grant program or government-backed loan.

Different Financing Strategies

“Right now, it’s a mental game for many potential buyers. They are struggling to overcome the mindset that they need to wait for rates to drop back to 3.75% so they ‘get the best deal,’ ” said Pulver. “The reality is we can still put together a great deal, it just requires different financing strategies.”

With prices pulling back and bidding wars dissipating, buyers can put some of the extra money they needed for a downpayment towards points, “buying down” the interest rate to something lower. Each point the borrower buys costs one percent of the mortgage amount. So, one point on a $300,000 mortgage would cost $3,000.

“At top of market, we had homes selling for $100,000 over asking price. We’re not seeing that anymore,” said Pulver. “Think about the extra cost of the downpayment funds and financed amount in a situation like that. You can buydown the rate significantly with that savings. The buydown can lower the monthly payment and reduce the interest paid over the lifetime of the loan.”

What Should Buyers do Now?

To be prepared, prospective buyers whould stay engaged in the homebuying process. Although many people did need to “take a break” after some disappointments, you never know when an opportunity may occur and it’s best to be prepared:

Stay in Touch with Their Lender – Reach out and make sure you are (still) prequalified or preapproved. Make sure to update your application with any changes to your financial position. Think about salary increases, new employer, additional loan you may have signed for (auto, furniture, etc.) or any other changes.

Revisit Their Wish List– Go back and consider what you wanted in your home and go over the rank order of those items again. With the experience you gained from past house-hunting activities, look at current properties on the market with a fresh eye.

Look at Today’s Numbers and Don’t Look Back – Talk to your lender or use an app to begin looking at numbers with today’s interest rates and home purchase prices. So much has changed, make sure you are looking at your purchase numbers with up-to-date information. Pulver advises people not to get caught up in past numbers. Move forward with a clean financial slate and mental slate.

Trend or Temporary?

It may be too early to tell if we are entering a new phase of the market or a temporary condition. But being prepared remains critical to making a home purchase as the market evolves.

“There is definitely a different environment out there at the moment. We’re keeping a very close eye on inventory numbers and rates,” said Pulver. “The buyers who are the best prepared are the ones who may really be able to benefit from some of the uncertainty. Whether it’s the start of a trend or a brief moment, buyers should be prepared. You have the best opportunity to take advantage of any opportunity that appears when you know your position.”

If you are ready to begin looking to purchase a home, please reach out to GRB’s mortgage team.

GRB’s Senior Vice President, Residential Mortgage Manager Mike Pulver weighed in on a recent Rochester Business Journal article regarding rising interest rates and the state of Rochester’s residential mortgage market.

Mike Pulver SVP, Residential Mortgage Manager

While the Mortgage Bankers Association (MBA) is predicting a drop of as much as 40 percent in mortgage originations due to interest rate increases and less refinance business, Pulver notes in the article that there is still a robust purchase market locally.

“We’re on track to do as much business this year as we did last year because we weren’t reliant on refinance business,” said Pulver.

While national lenders are already instituting layoffs, community purchase-money lenders like GRB remain stable from a staffing perspective. For buyers and Realtors, this means the bank is able to maintain turnaround times for processing and underwriting to ensure purchases close on time.

If you want to see the complete article, go to the RBJ’s website (you may need a subscription to access the article).

To reach GRB’s mortgage team, go to our website or call 585.427.9200.

First seen in Spring 2022, the META Information Stealer malware is becoming a popular cybercriminal tool. It is designed to steal cryptocurrency assets and passwords commonly stored in web browsers like Chrome, Edge, and Firefox.

In this campaign, criminals employ a standard lure of sending Excel spreadsheet files laced with malware macros as attachments to their targets’ inboxes. The email message usually mentions fund transfers to trick users into downloading and opening the attachment on their devices.

Once opened, the document prompts targets with a DocuSign message meant to deceive them to “enable content.” Then, a malicious VBS macro starts running in the background.

While there is a lot more to how this insidious piece of malware operates and protects itself from removal (see articles on BitDefender or Cyber Intel Mag for detailed information), this is a good time to reiterate some best practices for email security:

Be suspicious of attachments. Only open attachments from trusted sources. Ignore common traps like “funds transfer,” “take action immediately,” “critical action required,” etc.

Saving passwords in web browsers is convenient, but it does create a risk of compromise via a malware attack. Using a third-party password manager is a better solution.

If your system does become infected, seek professional assistance to ensure the malware gets completely removed. Malware uis often designed so that it can re-infect your system and/or avoid regular virus scans.

Keep up to date on current threats by subscribing to cybersecurity newsletters and resources.

Expect more attacks using META and similar info stealers. They work often enough to deliver financial results to the criminals that use them.

National Homeownership Week was established in 1995 and expanded to National Homeownership Month in 2002. The month-long celebration reinforces the belief that owning a home is a critical step towards achieving the American dream. The history of homeownership assistance in the U.S. involves access to financing and incentives. This assistance helps make the purchase of a home possible for a wider range of buyers. Since the 1800s, key government initiatives for housing support include:

Establishing the U.S. banking system with the 1860s National Bank Acts, making home mortgages available for the first time.

Creating the Home Owners’ Loan Corporation in 1933, the Federal Housing Administration in 1934, and the Federal National Mortgage Association (now known as Fannie Mae) in 1938 to stabilize the housing market during the Depression. In its 87 years, the FHA has helped more than 44 million citizens to become homeowners.

Creating the G.I. Bill of 1944, providing for subsidized mortgages for the veterans of World War II.

Passing the Fair Housing Act of 1968, banning discrimination in housing based on religion, race, gender, and national origin.

Homeownership by the Numbers

While we have come a long way, opportunity remains to expand the ability to build wealth through homeownership.

30% – Nearly 1/3 of American households devote more than 30 percent of their income to housing costs.

50% – Eleven million renters spend more than half their household budget on a place to call home.

2 Million – Two million seniors spend more than 50 percent of their income on rent during their “golden years.”

37 – For every 100 extremely low-income household, there are just 37 affordable rental units available.

New Housing is Expensive

The rising price of new housing developments is one part of the problem. In 2017, Fannie Mae estimated the average cost of building a one to three story apartment to be $192 per square foot. This represents a 30% increase from 2013.

This often translates into rents between $1,500 and $2,000 a month.

Families need to earn $60k – $80k per year to afford that, which is beyond the reach of low-to-moderate income consumers.

Why the Squeeze?

Experts, like the Federal Reserve, say this housing shortage is due in part to zoning and land use regulations that limit available space for development.

As a result, fewer multi-family and low-income housing units are built.

Banks Are Making a Difference

Banks understand that affordable housing requires more than making a loan. It takes flexible capital and cooperative relationships with consumer groups, nonprofits, and government agencies to foster community development. To help meet these housing needs, banks work with:

Nonprofits and Community Development Financial Institutions (CDFIs) to provide products with flexible underwriting standards and technical assistance.

State Housing Finance Agencies (HFAs) to secure low interest rates, low down payment mortgages and closing cost assistance for low-and moderate-income buyers.

The Department of Housing and Urban Development (HUD) to participate in their Rental Assistance Demonstration (RAD) program and Home Investment Partnership program (HOME).

Government Sponsored Enterprises (GSEs) like Fannie Mae, Freddie Mac and the Federal Home Loan Banks to access funding for well-priced single family and multi-family loans and to participate in the Affordable Housing Program (AHP) and the Community Investment Program (CIP).

Get Started with GRB

GRB provides government-backed loans (USDA, VA and FHA) to provide low down payment lending options. GRB is also an active participant in the Federal Home Loan Bank of New York Homebuyer Dream Program (HDP). HDP provides down payment assistance and counseling services for low- to moderate-income homebuyers. Collaboration between banks and housing-focuses agencies helps those in need find a place to call home in a challenging market.

If you’re considering a home purchase, contact GRB’s Mortgage Team to get started. As a community bank, GRB focuses on the growth of this region. Through our wide range of home lending options, GRB commits to supporting homebuyers during National Homeownership Month – and every day!

We are proud to announce that GRB has been recognized by the Independent Community Bankers of America (ICBA) as one of the “top-performing community banks of 2021” in the most recent edition of “Independent Banker” magazine. Ranked at no. 21 in the $300 million to $1 billion asset category, GRB is the only Western New York bank on the nationwide list.

ICBA’s calculations aim to recognize community banks that are consistent high performers. Using FDIC data, ICBA looks at pre-tax return-on-assets (ROA) figures from the past three years. Only four community banks in New York were part of this year’s ICBA list of 75.

In an interview conducted by Independent Banker magazine, GRB President and CEO Philip Pecora attributed GRB’s success to helping small businesses through its Small Business Administration (SBA) lending activities, exponential growth in the bank’s mortgage business, and significant investments in technology.

“We focused on technology to handle the transaction side of our business, to make the back end seamless. That allows us to focus on the personal side of the business,” said Pecora. “What differentiates us is the personal relationships, but the technology is a must-have.”

Being recognized for our profitability is certainly a significant achievement. But it would not have happened if not for the extraordinary efforts of the entire GRB employee team through some very challenging times. Our ability to move forward and still focus on our sales and service goals was critical for the bank and for its customers.

New York State “Business Person of the Year” Steven Olschewski of The Clubhouse Fun Centers.

During National Small Business Week, we are thrilled to extend our sincere congratulations to Steven Olschewski, owner of Clubhouse Fun Centers in Greece and Henrietta. Mr. Olschewski was named U.S. Small Business Administration district and New York State “Business Person of the Year” during this year’s celebration of National Small Business Week. This is the first time in 25 years the SBA award has been received by a Rochester, N.Y. business.

County Executive Adam Bello, Congressman Joe Morelle, and Victoria Reynolds, SBA Deputy District Director, presented the award to Mr. Olschewski and his wife, Marsina. The award recognizes Mr. Olschewski’s perseverance during the pandemic and the subsequent recovery of his family fun center business. After purchasing the Greece location in 2018 with an SBA loan from GRB, Mr. Olschewski ended 2021 with both locations having their best year yet. Mr. Olschewski was nominated for the award by Lydia Birr, Sr. Economic Development Specialist with the Monroe County Economic Development Office.

“Small business owners like Steven are tough as nails. Their drive, determination and ability to take calculated risks while also tapping into a pool of resources available for help, build a better economy in Western New York and we salute them during National Small Business Week,” said SBA Buffalo District Director Franklin J. Sciortino. Congratulations, Steven and Marsina!

At GRB, we celebrate small business every day. We’re a small business and we are deeply engaged with the small business community here in the Greater Rochester region.

We know this community and understand its unique needs and opportunities. GRB has been the top U.S. Small Business Administration lender in Greater Rochester the last two years. We are proud of the hundreds of commercial clients whose innovative ideas and hard work fuel our local economy. We are grateful for their role in providing quality jobs and supporting charitable needs.

Entrepreneurship is the foundation of this community. We are proud to share the stories of some of our small business customers on our Customer Stories page.

Congratulations to our business owner clients and to all those who have had made the bold move to turn their vision into reality. To celebrate, we are offering a number of activities this week:

Check out our social media channels for small business facts. Please, feel free to share! #NSBW

Talk to your relationship manager about the latest GRB tools, products and services. We are happy to help you reduce costs, guard against fraud, and enhance your operations.

We are pleased to announce GRB has ranked no. 5 in the the medium employer (100-250) category for “Best Companies to Work For New York.” This is a significant achievement and we are incredibly proud of our employees for making GRB a great place to work and a great place to bank.

Awards for the “Best Companies” are based on feedback provided through employee surveys, which focus on:

Leadership & Planning

Corporate Culture & Communications

Role Satisfaction

Work Environment

Relationship with Supervisor

Training, Development & Resources

Pay & Benefits

The survey process is managed by Best Companies Group (BCG) and winners are published by New York State SHRM (NYS-SHRM).

This year marks the ninth time GRB has secured a spot on the Best Companies list.

The idea of “sustainability” is linked to a lot of local activities these days. We reuse and recycle products, make purchases at a local bakery, and choose to buy American-made products. We know this supports our national economy. In turn, there are plenty of reasons why eating, dining, and banking locally makes good economic sense. Community Banking Month is the perfect time to reflect on banking locally.

If you’ve ever wondered if it matters where you deposit your hard-earned money, let me assure you it does. Banking locally certainly supports small businesses. But that’s not its only contribution. As a locally owned and operated business, community banks are part of the economic engine that creates 62 percent of new jobs annually.

Community banks put people first

Community banks like GRB take in deposits and distribute loans that feed into a self-sustaining micro-economy. Our deposits and loans keep funds right here in Upstate New York. And the proceeds from those businesses employ residents, fund municipalities, and continue the cycle of locally based economic growth.

And if you need more proof, just consider the community bank response to the coronavirus pandemic. Community banks were the economic first responders. They made 60 percent of total Paycheck Protection Program loans to small businesses. During Community Banking Month, it’s important to note that as a group, community banks are:

The preferred small business lenders. Community banks maintain an 81 percent net satisfaction score. This compares to 68 percent for large banks and just 43 percent for online lenders.

Responsible for funding more than 60% of small business loans and more than 80% of agriculture loans.

Often operating in areas abandoned by others—serving as the only physical banking presence in nearly one in three U.S. counties.

Local benefits every day

But it is not just about stats. At GRB, our employees are empowered to find solutions to meet our customers’ goals. And when our employees log volunteer hours or when GRB contributes to local charitable organizations, we help ensure economic prosperity and quality of life.

April is Community Banking Month, and we thank our customers for putting their trust in us for their banking needs. For our neighbors who may be considering a switch, take a closer look at GRB. We pledge to never lose sight of the all-important “relationship” and the personalized service our customers expect. For more information, visit our Business Banking, Personal Banking and Home Mortgage pages.

Remember, we are all in this together. Community banks are only successful if our customers and communities are, too. We know what it takes to create successful local economies. Join us in helping to build a more sustainable, vibrant economy here at home! Bank local with GRB and celebrate Community Banking Month!

Follow our social channels for special Community Banking Month features throughout the month of April.

Financial advice is everywhere, but much of it falls into the realm of rumor, half-truth and speculation.

When talking about your finances, it helps to identify your goals and establish a plan that brings those goals closer to fruition. If you need help, look for qualified individuals (accountants, legal counsel, financial planners, etc.) to provide guidance. But in the end, the money is yours and you need to be comfortable with your plan.

Although financial decisions are not one-size-fits-all, there are some best practices. In honor of April Fool’s Day – and the beginning of U.S. National Financial Literacy Month – see if you can tell which of these statements are financial fact or a financial fool’s errand.

Fool. Saving is definitely a situation where every little bit counts. Saving just 15% of pretax income (including your employer’s contribution) can go a long way towards maintaining your lifestyle in retirement. Use the GRBbank Online Banking My Budget feature to track your monthly expenses and set savings goals.

Fact. A budget is the first step to financial success. Without a budget, spending can easily begin to outpace earning and leave the user in debt. A budget provides a benchmark that can be used for ongoing planning and to help meet financial goals. Check out the My Budget tool on GRBbank Online Banking.Add Accordion Item

Fool. While a good credit score does provide potential borrowers with more options, there are programs for credit-challenged individuals. Many lenders, like GRB, also provide credit repair services to help borrowers take the right actions to raise their credit score. While it still may require some time and patience, home ownership can still become a reality.

Fool. While easy and convenient, person-to-person payment apps have a couple of shortcomings. First, they are not insured. Financial institutions insure accountholders for up to $250,000. If the app goes down and your money disappears, there is no recourse. Apps also do not offer interest on the money left in user accounts. Look for high-yield accounts, like GRB’s Reward Checking account, and make your money really work for you.

Fool. Having a credit card and making timely payments can help build a favorable credit history. But carrying a balance is not part of that equation. A balance is considered revolving debt and factors in to your credit utilization, which can actually hurt your score., and make that interest work for you.

Fact. Why? Keeping a zero balance on a card improves your credit utilization ratio (revolving credit used divided by revolving credit available). As long as you aren’t being charged significant fees for the card, it may be more beneficial to keep it active.

Fool. Traditionally, home mortgages and student loans have the lowest interest rates and may even be tax deductible. Paying off higher-interest debt or even using that extra money to save for retirement is often more financially sound. Not sure? Talk to a financial planner or accountant.

How did you do? If you need some additional information, go to our Financial Wellness page for resources and tips for saving, credit repair, home buying, and more.